ARCHIVES

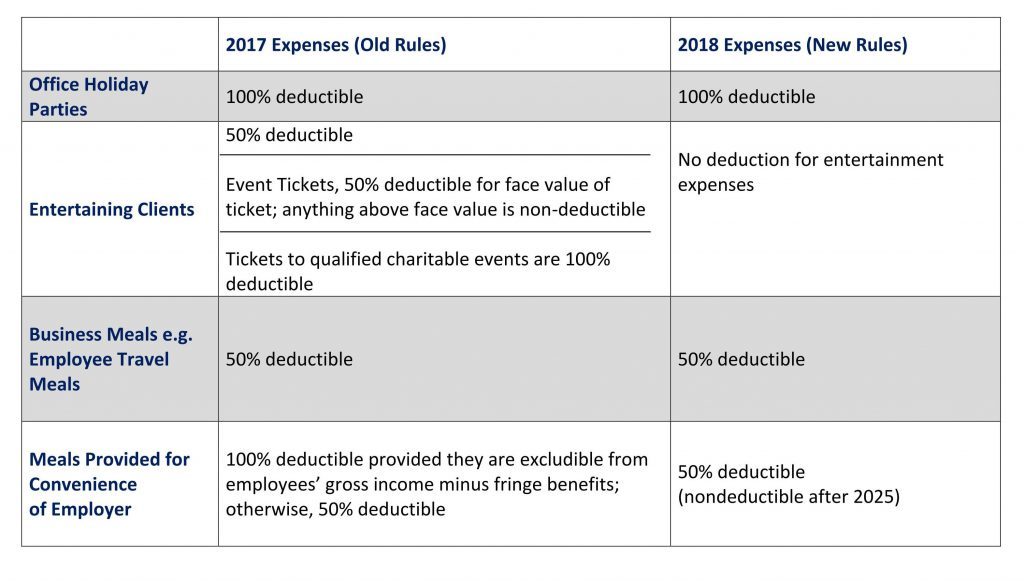

Under the new tax law there are stricter limits on deductions of business meals and entertainment expenses. Entertainment expenses incurred or paid after December 31, 2017 are nondeductible unless they fall under the specific exceptions in Code Section 274(e). One of those exceptions is for “expenses for recreation, social, or similar activities primarily for the benefit of the taxpayer’s employees, other than highly compensated employees”. (i.e. office holiday parties are still deductible). Business meals provided for the convenience of the employer are now only 50% deductible whereas before the Act they were fully deductible.

Businesses should keep these new rules in mind as they plan their 2018 meals and entertainment budgets. See below for a chart comparing the rules before and after the Act.