ARCHIVES

When it comes to managing financial and legal documents, there is no one-size-fits-all answer. Recordkeeping requirements can differ across business and personal records and can even vary by industry. When in doubt, it is always best to err on the side of caution and keep a document longer than the minimum required time.

If you’re looking for some general guidelines, we’ve gathered up some “best practices” for managing financial records.

General Recordkeeping FAQs

Generally speaking, you’ll want to keep your records organized and separate. That means financial records are separate from legal records and personal records are separate from any business documentation.

This ensures your records stay organized and are easy to access, but also helps to protect you in the event of an audit or legal action. Generally speaking, the more segmented, the better.

What Business Records Should I keep?

There are a few different types of financial documents that you should keep track of for your business. These include financial statements, receipts, invoices, and contracts.

Organizing your business documents can seem like a daunting task, but it makes life a lot easier when you need to reference the information down the road. Start by separating legal, financial, and operational information.

Keep all of your financial documents in one place and organize them by year or quarter, separating out any contracts, loan documentation, tax information, etc .

Still not sure where to start? Consider consulting with your accountant or CPA for best practices on managing your financial records.

Keep Permanently

- By-laws and corporate minute books

- Canceled checks

- Capital stock, bond records, proxies

- Cash books, chart of accounts

- Current contracts, mortgages, notes, leases

- Copyrights, trademark registrations, patents

- Legal and tax correspondence

- Deeds, easements, bills of sale

- Financial statements

- General Ledgers, year-end trial balance

- Current insurance policies

- IRS audit reports

- Journals, Labor contracts

- Property appraisals

- Property records (costs, depreciation, schedules, blueprints, plans)

- Retirement and pension records

- Tax returns and worksheets (any documents relating to determination of income tax liability), Current training manuals

Keep 7 Years

- Accounts payable and receivables invoices, ledgers, and schedules

- Bank statements, deposit tickets

- Expired contracts, mortgages, notes, leases, stock and bond certificates

- Expense reports, Insurance documents (settled claims, accident reports)

- Inventory records

- Notes receivable ledgers and schedules

- Payroll (time cards, earnings records, garnishments), Terminated personnel files

- Sales contracts

- Documents relating to payment to vendors and employee reimbursements

- Withholding tax reports

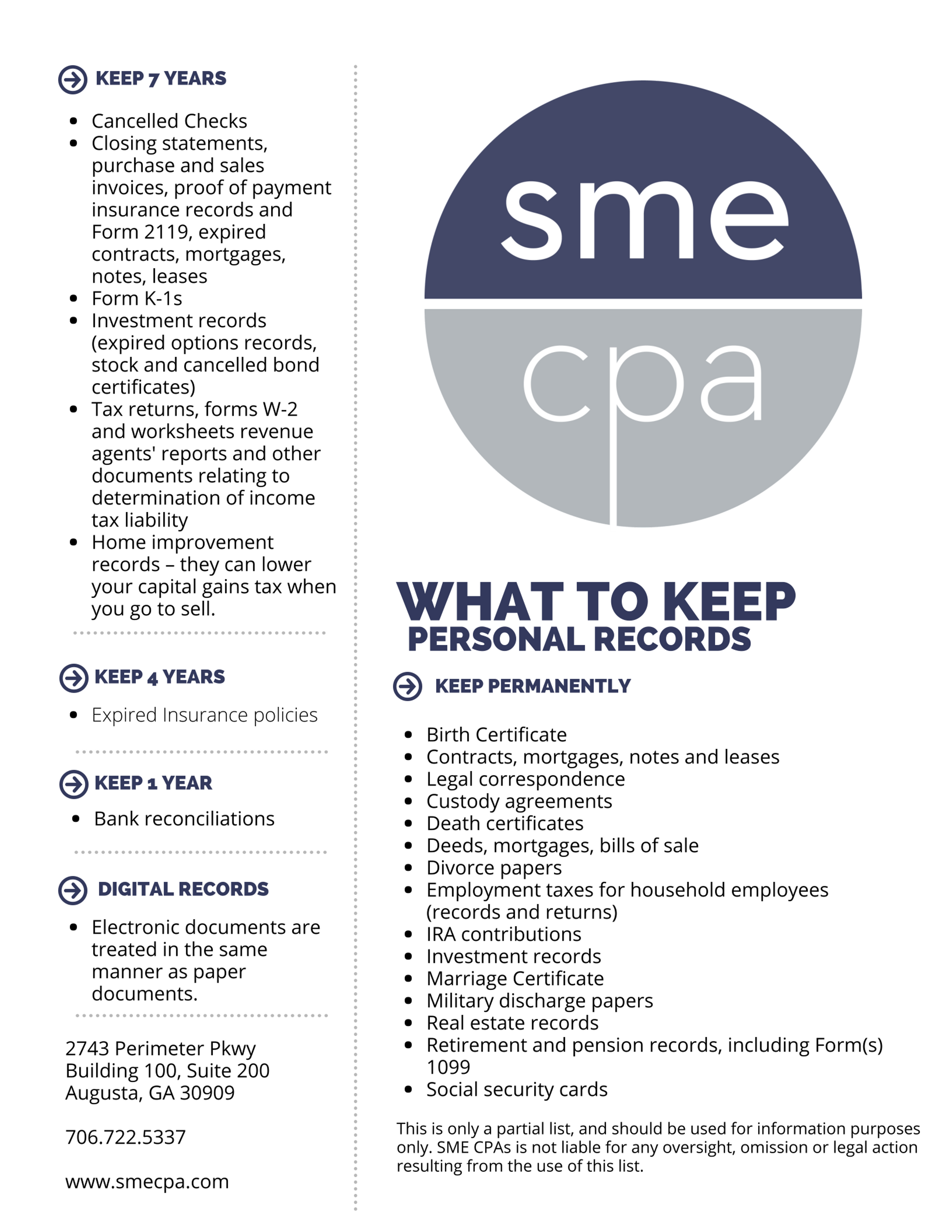

- Canceled Checks

- Closing statements, purchase and sales invoices, proof of payment insurance records and Form 2119, expired contracts, mortgages, notes, leases

- Form K-1s

- Investment records (expired options records, stock and canceled bond certificates)

- Tax returns, Form W-2 and worksheets, revenue agents’ reports and other documents relating to determination of income tax liability

- Home improvement records – they can lower your capital gains tax when you go to sell

Keep 4 Years

- Employee applications

- Expired insurance policies

- Petty cash vouchers, Internal reports

Keep 2 Years

- Bank reconciliations

- Correspondence with customers and vendors

- Purchase orders

- Purchase and sales requisitions

- Shipping and receiving documents

Keep 1 Year

- Bank reconciliations

Digital Records Reminder: Electronic documents are treated in the same manner as paper documents.

What Personal Records Should I keep?

Not sure what to keep and what to toss when it comes to managing your personal records and financial documents? Here’s what you need to know.

{kind=link}

Keep Permanently

- Birth Certificate

- Contracts, mortgages, notes and leases

- Legal correspondence

- Custody agreements

- Death certificates

- Deeds, mortgages, bills of sale

- Divorce papers

- Employment taxes for household employees (records and returns)

- IRA contributions

- Investment records

- Marriage Certificate

- Military discharge papers

- Real estate records, Retirement and pension records, including Form(s) 1099

- Social Security cards

Keep 7 Years

- Canceled checks

- Closing statements, purchase and sales invoices, proof of payment, insurance records and Form 2119, expired contracts, mortgages, notes and leases

- Form K-1s

- Investment Records (expired options records, stock and canceled bond certificates)

- Tax returns, Form W-2 and worksheets, revenue agents’ worksheets and any forms relating to income tax liability

- Home improvement records (these can lower your capital gains liability during a resale)

Keep 4 Years

- Expired Insurance policies

Keep 1 Year

- Bank reconciliations

Digital Records Reminder: Electronic documents are treated in the same manner as paper documents.

How to Safely Store Your Documents

Safeguarding your personal and business information is important for a few reasons. First and foremost, it helps to protect the integrity of your information. Second, it ensures that in the event of an audit or legal inquiry you’re prepared with the necessary information to protect yourself and your business.

Storing your documents in a safe place helps to protect them from theft, damage, and loss. There are a few different ways that you can store and safeguard your personal and business information, including:

- Storage in a locked filing cabinet or restricted access file room

- Storage in a safe deposit box

- Storage at an off-site records storage facility

- Encrypt your digital and electronic records

What to do with documents you no longer need?

Depending on the type of information your business manages, there are compliance regulations you must follow when it comes to disposing of documents. These include the Health Insurance Portability and Accountability Act (HIPAA), the Gramm-Leach-Bliley Act (GLBA), and the Sarbanes-Oxley Act (SOX).

When disposing of documents, businesses need to make sure that they follow the guidelines set forth in these compliance regulations. This includes shredding or burning any documents that contain financial information, personal information, or medical information.

Shredding your documents is the best way to dispose of them because it ensures complete destruction of your records. You should shred any documents that contain financial information, such as bank statements, credit card statements, and tax returns.

Burning your documents is another option for disposing of them. You should burn any documents that contain sensitive information, such as financial information, medical information, and personal information.

What not to do when disposing of documents:

- Do not throw your documents in the trash

- Do not recycle unshredded documents

- Do not leave your documents in a public place

Reminder: if your business closes, you are still responsible for managing the security and final destruction of any business or personally identifiable information possessed by your business, in accordance with the retention requirements of your industry.

Need Specific Guidance

If you are looking for specific guidance on document retention requirements specific to your organization and industry, talk with a compliance officer, your CFO, or your CPA. They will be able to advise you on which documents you are required to keep and for how long.